NBER declared that the US entered a recession in February, using labour statistics and monthly PCE to make their decision.

COVID figures are rising in the US, with a 'second wave' feared in the media; this is still the first wave.

Looking at the data, COVID cases in Mexico, Brazil & Saudi Arabia are currently on a more alarming trajectory than that of America, though it is only nearer the end of June that the size of spike in cases due to protests will become apparent.

Sweden is also concerning, now near the top in confirmed cases per million with a clear upward trajectory.

Protests continued in many developed nations, though with a move towards defacing historic statues and a reduction in overall violence.

Brexit grind continues

0300 : CNY China Industrial Production, Retail Sales & NBS Presser

1600 : USD FOMC Member Kaplan Speaks

2200 : NZD New Zealand Consumer Survey & House Prices

The British PM & European Council & Parliament Members hold high level Brexit talks today. June marks the 4 year anniversary of the Brexit referendum.

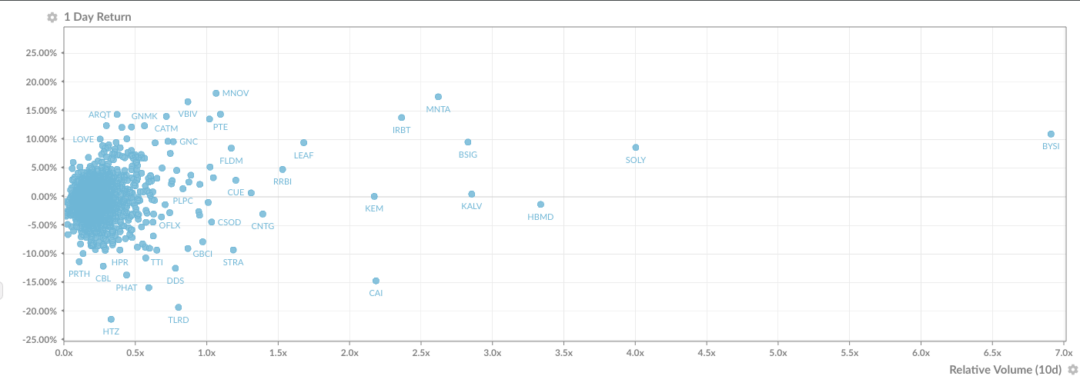

IS THE TOP IN?

Ned Davis Research put out a study recently that showed equity markets bottom on average 4 months before the end of a recession. Small caps always lead the bounce.

The Russell 2000 fell away from its lead last week & the days ahead are pivotal - if it remains pressured and EM's join it at the bottom, this goes some way to confirming the case for another leg lower.

However, that would signal that the US will only come out of recession in October or November. The only way that this would be the case is if the US goes back into full lockdown. This isn't to say that the recovery will be quick but that while the economic outlook may be dire, history tells us that risk markets have never cared. Is it really different this time?