The Pound initially had a little boost as the BOE was not as dovish as expected. The new BOE governor confirmed these ideas later, saying that negative rates and YCC weren't discussed.

£1 - worth less today due to BOE announcement

However, soon after the ramp up price reversed and Cable looks to finish over 1% down.

USD was strong across the board today and it remains to be seen if this was just rebalancing or a hint of a risk off move brewing

The next stimulus bill is going to be hotly contested; divisions within the Republicans are brewing and the Democrats are in control of the House.

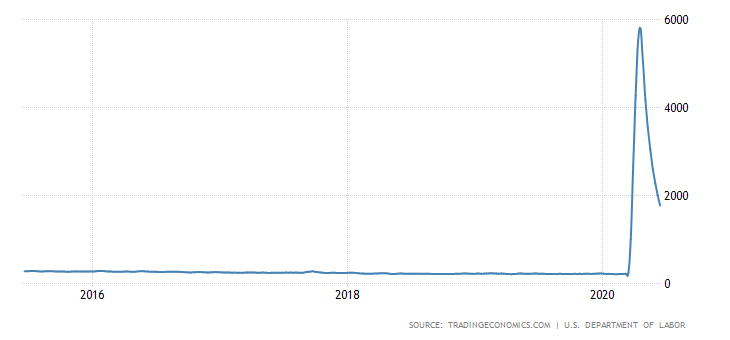

US Jobless Claims

With US Jobless claims remaining elevated today despite the 're-opening' (1.5mln v's 1.3mln exp, prev 1.5 mln) & the current round of stimulus cheques stopping in July, the market is increasingly concerned that the remaining strength of the US economy, driven by government spending, is going crumble.

weekend risk

0230 : AUD Australian Retail Sales

0700 : GBP UK Retail Sales

1330 : CAD Canadian Retail Sales

1800 : USD Fed Powell speech

Also due: European Council Meeting & BoJ Monetary Policy Meeting Minutes. Not many inputs; the main question mark is whether the market tilts risk off in preparation for the weekend or not.

NEW RECORD WEEKLY CLOSE FOR NASDAQ?

The Dollar was strong today bu US Yields sold off. Copper jumped early on and gave back all its gains. Oil moved higher but that could be down to the spiking COVID numbers in Saudi Arabia and expectations of more supply side issues.

European equities were lower but US equities have held up surprisingly well. With some major headline risk going into the weekend, it would be a feat for NASDAQ to close at new weekly all-time highs. It would need to fall over 2% tomorrow to move back below the last record weekly close.

The equity market continued its grind higher and volatility dripped down again.

Fed's Bostic was positive on jobs coming back & Powell reiterated that more support from Congress was needed. He also made the point that any curb in main street benefits would curb spending in the economy. Headlines surrounding any delays in the next round of US stimulus may dent risk appetite.

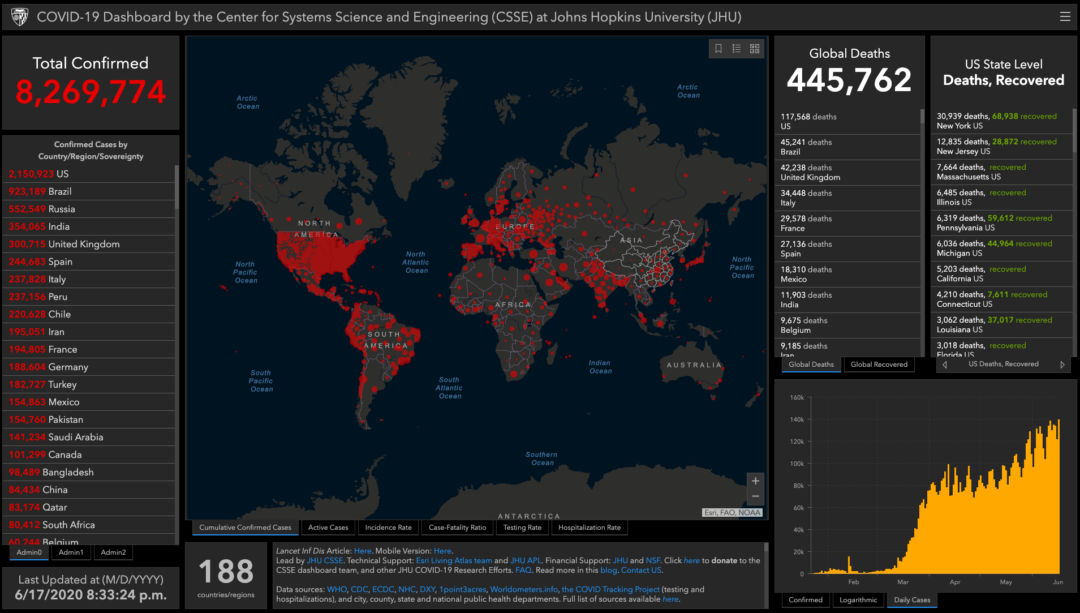

COVID cases continued to spike in the US. We all know it is going to get worse; if the market wanted to respond to this, it would already be lower.

COVID-19 - Daily Rates Still Going Up

If there begins to be hints of major shutdowns, this could change. For now, there is no expectation of full lockdowns and therefore only positive economic data is due in the coming months. Confirming this idea, Germany's finance minister Scholz said that there wouldn't be a full scale lockdown if there was a secondary outbreak in Germany.

DOES BOE SINK THE POUND?

0230 : AUD Australian Employment Data

0830 : CHF SNB Rate Decision & Policy Assessment

0900 : EUR ECB's New Economic Bulletin

0900 : CHF SNB Pres Conference

1200 : GBP BOE Rate Decision & Minutes

1330 : USD Jobless Claims & Philly Fed Manufacturing Index

1830 : CAD BoC's Schembri speech

CABLE COULD LEAD THE WAY

The 2019 open, around 1.276, has become a pivotal area. Cable looks to be backing off and into the recent range between 1.215 and 1.265. However on Monday, amid a boost in risk on, it held around 1.26 and has yet to make a decisive break lower.

The Pound

The argument for USD bears is that due to the massive amount of stimulus the Fed & US government has loaded into the system (and still promise to do more), the USD will weaken. With BOE expected to add more stimulus tomorrow, if Cable holds up it will be a sign that USD has lower to go.

Today had potential for volatility with a heavy news schedule and fireworks were certainly present in the afternoon.

US COVID cases are jumping higher, with Texas hospitalisations hitting a new record and Arizona new cases up 6.5% v's 2.8% expected and Beijing is raising its alert status amid a new outbreak.

In his testimony, Powell indicated that corporate bond buying is more of a contingency rather than something the Fed will carry out aggressively.

Though there was a major drop in risk, with SP500 at one point dropping around 3% from the highs, most of the move has been recovered, helped by more rumours of a new $1trn+ stimulus planned from the US government.

The Vix is still drifting through the 11th June spike, though overall price ranges are higher than the rest of the risk rally so far - an ominous sign.

Consumer Price Index DAY

0700 : GBP UK CPI

1000 : EUR European CPI

1000 : EUR ECB's Mersch speech

1200 : EUR ECB's De Guindos speech

1330 : CAD Canadian CPI

1330 : USD US Building Permits

1700 : USD Fed's Powell testifies

2345 : NZD New Zealand GDP

OIL SHOWS WEAKNESS

All risk assets took a hit today at a key moment, particularly oil which was breaking out of consolidation and past the last failed reversal in the March drop.

Follow through in oil tomorrow will add to the bearish tint in the market that has been holding heavy since the Fed last week.

USDCAD is unchanged on the day and if the oil is heavy tomorrow, this could give CAD another bout of weakness.

The reliable pattern seems to be back, for now, with a heavy close last week carrying through to early trading in the new week, sucking in some more liquidity to the downside before a harsh reversal.

Today it looks to have been helped by an updated Fed corporate bond purchasing plan and slightly lower new cases % in Florida but it is really just the rhythm the market has been playing all year.

The test will come later in the week as the weekend risk nears again.

There was little other news, however tomorrow there is a flurry of macro data.

Copper

It is worth noting the increased volatility and also that, as of yet, Copper looks to be finishing negative despite the risk rebound. Bonds are also relatively unchanged on the day; still signs of potential trouble ahead.

EVER PRESENT FED

0230 : AUD RBA Meeting Minutes & AUD House Price Index

04:00 : JPY BoJ Monetary Policy Statement (tentative)

0700 : GBP Unemployment Rate

0700 : EUR Ger CPI

1000 : EUR Ger ZEW Survey

1330 : USD Retail Sales

1500 : USD Fed's Chair Powell testifies

2000 : CAD BoC's Wilkins speech

2330 : USD Fed's Clarida speech

CAN BONDS HOLD THE LINE?

US Yields attempted to break the other way early June but were quickly hammered down and now sit on the verge of heading lower again.

US10Y Yields

Potential yield curve control aside, in the current environment an initial break lower would be seen as at least part confirmation that the bond market isn't buying that this risk rally has any further to go.

NBER declared that the US entered a recession in February, using labour statistics and monthly PCE to make their decision.

COVID figures are rising in the US, with a 'second wave' feared in the media; this is still the first wave.

Looking at the data, COVID cases in Mexico, Brazil & Saudi Arabia are currently on a more alarming trajectory than that of America, though it is only nearer the end of June that the size of spike in cases due to protests will become apparent.

Sweden is also concerning, now near the top in confirmed cases per million with a clear upward trajectory.

Protests continued in many developed nations, though with a move towards defacing historic statues and a reduction in overall violence.

2200 : NZD New Zealand Consumer Survey & House Prices

The British PM & European Council & Parliament Members hold high level Brexit talks today. June marks the 4 year anniversary of the Brexit referendum.

Russell 2000 Small Cap Index

IS THE TOP IN?

Ned Davis Research put out a study recently that showed equity markets bottom on average 4 months before the end of a recession. Small caps always lead the bounce.

The Russell 2000 fell away from its lead last week & the days ahead are pivotal - if it remains pressured and EM's join it at the bottom, this goes some way to confirming the case for another leg lower.

However, that would signal that the US will only come out of recession in October or November. The only way that this would be the case is if the US goes back into full lockdown. This isn't to say that the recovery will be quick but that while the economic outlook may be dire, history tells us that risk markets have never cared. Is it really different this time?