So far, it has certainly been a buy the rumour sell the fact after FOMC yesterday with all equities down heavily on the day. Powell said the same support would be there- but didn't over-promise & left yield curve control as a distant option.

Elsewhere, Copper fully reversed the break upward from yesterday and in FX, commodity currencies completed the strong risk off environment, falling heavily.

Trump tried to blame the Fed (he seems to be giving China a break for the time being) & the White House voiced the idea that the next stimulus package could be out in July.

That's the one issue with a disorderly selloff; it puts pressure on the US government to approve stimulus quicker than planned & that could cut the drop short, at least for a strong intermediate rally.

However, overall, the tide has turned.

VIX wakes up

Going some way to confirm the force of the sell off, the Vix jumped to levels not seen since early May & currently looks to be closing near the highs.

If the selloff continues in the next sessions, it is highly likely that there will be some retracement early next week in a similar pattern to the first selloff this year.

This should provide another opportunity to short so we wouldn't look to be aggressively short into the weekend unless there is a retracement early tomorrow.

Against a backdrop of a worldwide pandemic & riots, the US tech. index has breached 10,000 for the first time.

Aside from the NASDAQ, equities were quite weak, with European equities closing lower and SP500 looking to do the same.

It was an odd up and down day, with oil moving from over 2% down to closing at the highs, around 2% up.

Gold was up more due to heavy USD weakness than anything else. Yields had a bad day and that supported Yen & Swissy strength. Commodity currencies were weak, though well off the lows now.

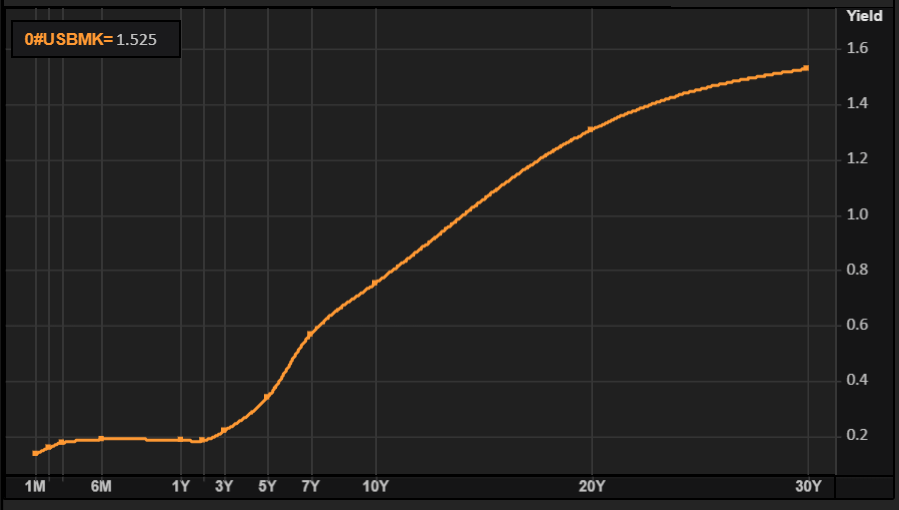

The market is signaling caution, though this could just be due to apprehension over the FOMC meeting tomorrow.

EVERYTHING LINING UP

We can add EURUSD to the list of currencies in key areas as we head into FOMC, with the highs today getting within 100 pips of the 2019 open - which has also been a key historic area of liquidity.

FOMC

Like so many other currencies v's USD, it is extended on its run & even if this is a major breakdown for USD, a big spike tomorrow could set up a fade that would work even if only to re-test the 1.13 area. With the market freezing up slightly today and everything in such important areas, tomorrow may be a pivotal moment for the coming months.

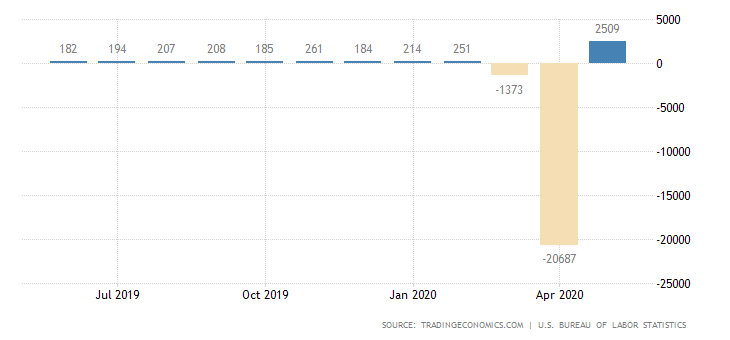

NFP estimates were miles off the mark on Friday. The old cognitive bias is kicking in strong for economists in this turbulent time and I doubt it is the last major deviation we will see in the coming months - though this was certainly a large one.

The initial reaction was a further jump in equity prices & general risk on mood, however it was noticeable how little AUD participated, grinding slightly higher whereas oil was up over 5% & various indices up 2% or more.

Riots continued in the US over the weekend, though were less violent than many perhaps expected, with Trump ordering the National Guard to leave D.C. & New York ending its curfew.

OPEC+ agreed to a month-long extension, with promises that the lack of compliance from some members would be made up. WTI has now made over a 200% rally off the lows & with the extension largely expected and priced in, it may come off in the week ahead.

Weakness In Gold

Gold had a poor week, with its lowest weekly close since March. This was also during days when USD was falling away which should support Gold.

Longer term, Gold is likely to move higher but for now we have everyone piling in to the trade, possibility of better news ahead meaning less monetary stimulus & if it does all fall apart, we know that Gold will be liquidated in a major sell-off. Make or break time this week & we are leaning towards a breakdown.

While the market was waiting for the ECB to be out of the way, the real news continues to be Germany's willingness to keep the purse strings open, with Merkel getting further stimulus approved yesterday & furthermore, hopes of closer fiscal union between the whole of the EU still alive. The UK was one of the main forces standing in the way of closer fiscal union; just perhaps, the UK leaving strengthened rather than weakened the Euro, at least for the next few years.

In saying that, this initial move has been significant and has potential for a heavy pullback, particularly if the US gets its act together. However, just while Europe is completing its re-opening, with reports from Scandinavia that life is 'back to normal,' areas of the US are seeing jumps in COVID cases again. While COVID numbers haven't been the thing to watch for a while, US numbers need to be kept an eye on over the next few weeks.

Following the European Central Bank's (ECB) decision to expand its Pandemic Emergency Purchase Programme (PEPP) by €600 billion to €1,350 billion, Christine Lagarde, President of the ECB, is delivering her remarks on the monetary policy outlook in a press conference.

Todays ECB bullet points:

• ECB still faces risks of fragmentation.

• ECB capital key is benchmark for purchase programs.

• PEPP operations will continue to operate flexibly.

COPPER: POP OR DROP?

Similar to other instruments, Copper has almost retraced its full March drop. Today was weak & failed to make a new high at the key 2.5 area.

With weekend risk ahead, there are a few signs that a retracement in risk is on the cards in to FOMC next week. If Copper drops lower early tomorrow, long Yen starts to look more attractive.